In a fiercely competitive telecom landscape Mobile Virtual Network Operator (MVNOs) are budding up pretty quickly, as they make better business sense. MVNOs essentially resell voice and data services of a larger operator. Several reasons why MNO’s allow such MVNOs to leverage their network are: Focus and serve a target/niche segment, Generate economies of scale for better network utilization, Increase Revenue, Service Differentiation, Overcome Govt. Policies that hinder flexibility & growth, Acquire new customers and last but not the least expand market.

According to GSMA Intelligence, as of the end of 2015, the world’s Mobile Network Operator (MNOs) hosted 1038 MVNOs and 277 MNO sub-brands. And the trend is set to gain more steam. According to latest estimates, the global MVNO market is expected to be worth USD 73 Billion and the number of subscribers to exceed 300 million, growing at a CAGR of 10% by 2020.

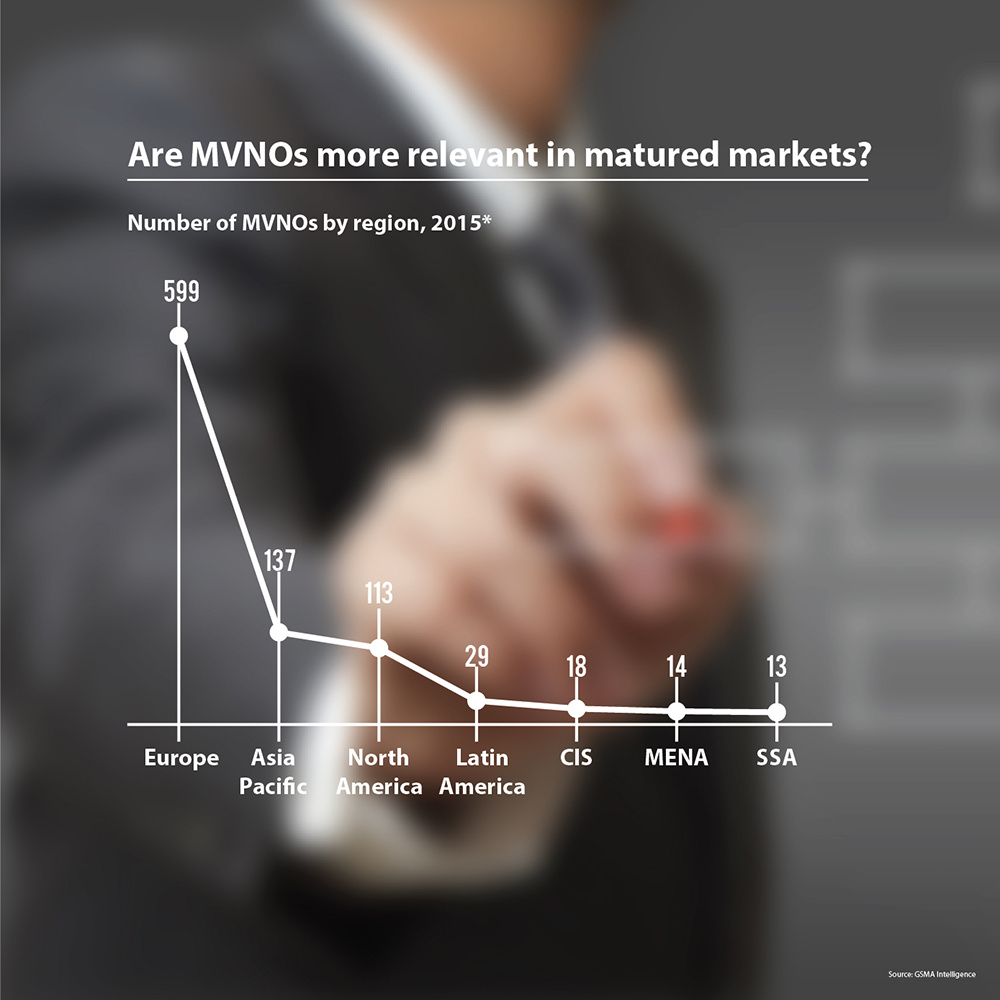

Out of the 1300 MVNOs across the globe, Asia Pacific (137) is second to Europe (599) in terms of global MVNO footprint followed by North America (113). In contrast the Sub-Saharan Africa has the lowest MVNO operators with just 13 MVNOs across the region. It is clearly evident that MVNOs are a phenomenon in the developed world as 4 out of 5 operators belong to such markets. The inference is perhaps, mature markets have more segmentation and evolved needs supported by policy and intention.

1 out of 3 MVNO in the world belong to Europe, with Germany leading the pack with more than 140 MVNOs followed by the UK. Markets such as Spain, Denmark, Belgium, and the Netherlands are fast gearing up. The success can be attributed to the tremendous increase in mobile data usage driven by high penetration of smart phones, deployment of high speed 4G networks, favorable regulatory guidelines and rising demand for VAS services.

Asia Pacific region has shown some momentum as regulators have liberalized their policies and invited operators to procure MVNO license. Expectation is to increase competition, reduce price and introduce innovative services in the market. China has liberalized their MVNO policy in 2014, whereas India and Malaysia have also passed MVNO specific laws. Countries such as Australia, Japan, Singapore, Philippines, Myanmar, and Thailand are also evolving in terms of virtual operators. The increase in the number of operators is attributed to the large subscriber base, high penetration of smart phones, deployment of high speed 3G/4G networks, favorable economic conditions that supports MVNOs framework.

MVNO in the Middle East, even though a developed economy has a very limited presence, and lags behind regions such as Europe and North America. Oman and Saudi Arabia are the early adopters in launching MVNO services in their respective markets. According to Pyramid Research the total MVNO subscriptions in the Middle East (including Oman, Jordan, Saudi Arabia and Israel) to grow at a CAGR of 19.5% to reach 7.3m in 2020. The reason for limited operators in the region is attributed to high barriers to entry due to oligopolistic market structures, unfavorable regulatory policies, regulation of tariffs, and high risk, in short, more to do with geo-political factors than the market.

North America will continue to grow in terms of MVNO demand, as all the big players are actively involved. Moreover, the MNO model is also near saturation. Latest technology, attractive commercials, favorable regulatory framework are a few key reasons that could be attributed to the success of MVNO in North America.

Latin America, on the other hand, lags far behind, though, it has shown tremendous potential for MVNOs to flourish. Countries like Mexico, Chile, Colombia, Peru and Argentina have shown strong momentum. LATAM is one of the very few markets where Tier 1 operators are themselves interested in launching MVNO in their respective territories. However, LATAM has its own set of challenges i.e. declining ARPU, income disparity, unfavorable regulatory framework, dysfunctional political processes, lack of spectrum availability etc.

MVNOs have failed to set foothold in the Africa Region. The failure can be attributed to unsupportive regulatory guidelines, low ARPU, very small difference between wholesale and retail rates. Kenya and South Africa are leading in the region with a modest number of subscribers on MVNO Network. However, the benefits that the MVNO model offers have forced other operators to consider it as a viable option. Regulators have taken steps in promoting favorable condition for MVNOs to operate.

Overall, the MVNOs are on the radar of each region but depending on market dynamism mixed with factors like policies, government structures, economy have bearing effect on the final evolution. But MVNOs are here to stay…that is evident.